Have you just recently bought a new home? Don’t get caught up in the excitement of closing payments and forget to protect your home by getting homeowners insurance.

According to ISO in 2018, 5.7% of insured homes had a claim, with 98.1% of the claims being for property damage, including theft.

Hence, what should come to your mind when you hear the words “homeowners insurance?”

Protection!

Look around you. Most people cannot afford to rebuild or replace everything in their home if disaster strikes. This is one of the major reasons why home insurance is crucial.

If you are a new homeowner in California and the surrounding regions, you shouldn’t leave your home to chance. You need to invest in a reliable homeowner insurance agency to secure your prized possessions.

To guide you, we have prepared an outline that will make it easier for you to understand the concept of homeowners insurance and why you should invest in it. Here’s what we’ll be talking about:

- The concept of homeowners insurance

- Major types of homeowners coverage

- What are your loss settlement options?

- Understanding limits and deductibles

- 7 Tips for reducing insurance cost

The Concept of Homeowners Insurance

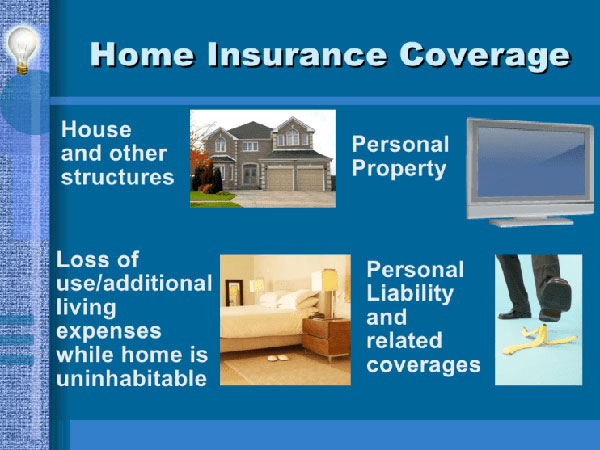

A homeowners insurance policy protects your home and belongings against unexpected loss. Hence, homeowners coverage protects your property, personal possessions, and you too.

When you buy a homeowners insurance policy, you’ll receive a package policy consisting of a combination of these major coverages:

- Dwelling

- Other structures

- Personal property

- Loss of use

- Personal liability

- Medical payments

- Flood insurance

- Earthquake insurance

- Water backup of sewer

- Personal umbrella liability

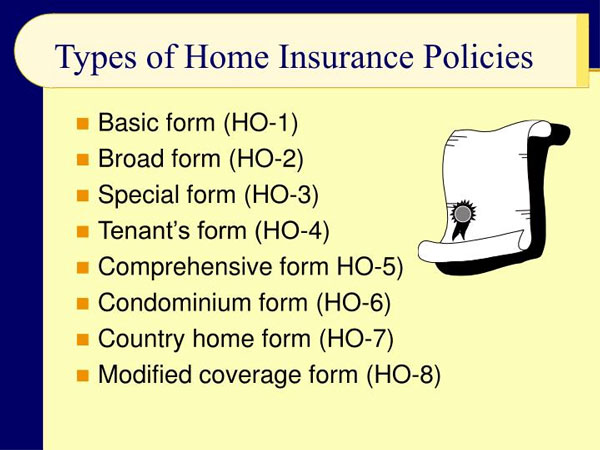

Major Types of Homeowners Coverage Policies

Homeowners insurance in the United States is available in several forms that are now regarded as standard in the industry. There are different levels of protection for each form to suit the needs of individual homeowners and their types of residences.

Of the eight known types of home insurance policies, we will focus on the ones suitable for owner-occupied dwellings:

1. HO1 coverage

The HO1 policy is the most basic homeowners insurance coverage that a new homeowner in California and Idaho areas can buy. It only pays for damages that are caused by the following 10 hazards:

- Aircraft

- Explosion

- Fire and lightning

- Riots and civil commotion

- Smoke

- Theft

- Vandalism and malicious mischief

- Vehicles

- Volcanic eruptions

- Windstorms and hail

2. HO2 coverage

In addition to the perils listed above, the HO2 policy also covers the following six events:

- Accidental discharge of water or steam

- Damage from electrical currents

- Falling objects

- Freezing of home systems

- Ice, snow, or sleet

- Tearing apart, burning, cracking, or bulging of home systems

An HO2 policy covers a total of 16 named risks that could cause damage to your home.

What about the countless other hazards that can damage your home?

To get broader coverage for your home, you need to get an HO3 coverage policy.

3. HO3 coverage

Unlike HO1 and HO2 that are “named perils” policies, the HO3 insurance policy for your home is an “open perils” type of policy. The open perils policy covers all risks, except those that are specifically excluded.

Acts of God and acts of war, such as floods and earthquakes are commonly excluded perils that will not be covered by a standard policy. You may have to get special coverage for them if you’ve just moved into an area that is prone to these natural disasters.

Most mortgage lenders only allow homeowners to buy HO3 policies at the minimum coverage, especially if they are single families, because it provides more home protection.

4. HO5 coverage

This type of coverage provides open perils, as well as replacement coverage for personal property. It is suitable for homeowners with many valuable possessions.

5. HO8 coverage

This provides repair cost coverage for dwellings incurring replacement costs far exceeding their market value.

What Are Your Loss Settlement Options?

How are you reimbursed for a loss?

Although most homeowners insurance policies have the same coverage components, the amount of money you are reimbursed or paid out for a loss will depend on the quality of your insurance policy.

The three major types of loss settlement options available for homeowners insurance are:

- Actual cash value

- Replacement cost

- Guaranteed/extended replacement cost

1. Actual cash value

Actual cash value is given after a loss to pay for the repairs or replacement of either your home or personal property, but without the cost of depreciation.

The depreciated value of your property is the amount the property is worth today in its present condition, not the same amount you paid initially.

2. Replacement cost

When your property insurance policy is one at its replacement cost, it means that there is no depreciation in your claim reimbursement.

What does this mean for me?

Well, if your personal property is either damaged or stolen, your insurance agency will reimburse you based on the value of the new items. In the same vein, if your home is either damaged or destroyed, the insurance agency will use materials similar in type and quality of your former home to repair or rebuild your house.

Most owner-occupied homes in the United States have a standard HO3 policy covering the home and attached structures at a replacement cost. Personal property, however, is set at a default to be covered at its actual cash value.

Hence, your insurance agency is likely to ask you to upgrade the terms of your personal property coverage loss settlement to replacement cost so that you will be liable for a slightly higher premium.

3. Guaranteed/extended replacement cost

Additionally, most insurance agencies offer guaranteed/extended replacement cost claim reimbursements to give you a coverage cushion in case the cost of rebuilding exceeds the policy limit.

Is guaranteed replacement cost different from the extended replacement cost?

Yes!

Guaranteed replacement cost is when you are paid out the rebuilding amount. Extended replacement cost, on the other hand, pays a particular percentage that exceeds your policy limit (often 25 or 50 percent) in case the cost of construction and labor are inflated after a disaster.

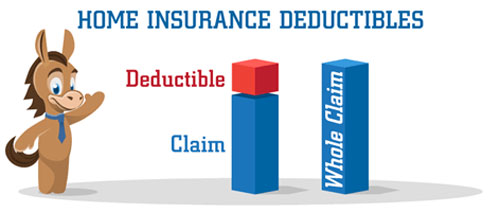

Understanding Limits and Deductibles

A homeowners insurance policy will not prevent your home or belongings from getting damaged, but it will provide a reliable financial safety net for you if something unexpected happens.

Bear in mind that coverage comes with both limits and deductibles.

Limits

Limits have to do with the maximum amount that your insurance policy will have to pay towards a covered claim. Some of the things to consider when selecting your coverage limits are the potential costs of either rebuilding your home or replacing some of your belongings.

By doing this, you will be prepared for covered perils such as fire and damage to your home or belongings.

Deductibles

Many types of coverage come with deductibles too. A deductible is an amount that you must pay before the insurance benefits kick in. You pay a deductible out of your pocket before your insurance agency reimburses you for the remaining loss.

The average U.S. home insurance premium, according to the National Association of Insurance Commissioners (NAIC), is $1,034.

Will you have enough money to pay a deductible out of your pocket should you need to lodge a claim?

Raising your deductible could save you up to 16% on your premium. Most policy deductibles range from $500 to $2,000, but certain agencies offer up to $25,000. Although high deductible policies are significantly cheaper than the low ones, it may be unaffordable if you are trying to file a claim.

If, for example, your insurance agency agrees to pay a claim settlement of $5,000 because your roof was damaged by a storm and your deductible is $1,000, you would first have to pay the deductible amount before your insurance agency sends you a check for the $4,000 balance.

7 Tips For Reducing Insurance Costs

Although it is not advisable to settle for cheap coverage, there are some other ways you can reduce your insurance premiums.

These seven cost-cutting tips can help you save more than 10% in premiums:

1. Get multiple policy discounts

Most insurance agencies offer discounts of up to 10% to customers with multiple policy contracts, such as buying homeowners insurance, health insurance, and auto insurance.

If you want to save on premiums, you should consider talking to your insurance agents about buying other types of insurance from the agency providing your homeowners insurance.

2. Increase your deductible

The higher your deductible as a homeowner, the lower your annual premiums. This principle also applies to car insurance or health insurance.

The problem with choosing a high deductible, however, is that claims such as broken windows that would not typically cost so much to fix is likely to be absorbed by you. All these factors can add up at the end of the day.

3. Maintain a good security system

If you install a burglar alarm that is monitored by your state’s central station or is linked directly to the local police station, you could be lowering your homeowners annual premiums by up to 5% or even more.

To get this discount, you will have to provide your insurance agency with proof in the form of a contract or bill showing that you have central monitoring in your home.

To further decrease your annual premiums, you could also install security alarms, smoke alarms, carbon monoxide detectors, sprinkler systems, weatherproofing, fire extinguishers, and dead-bolt locks. All these could help you to save up to 10% in annual premiums, especially when you are installing them in an older home.

4. Pay off your mortgage

Most homeowners take a very long time to pay off their mortgage. It is important to note that homeowners who own their residences are more likely to have their premiums reduced.

Why do homeowners who have paid off their mortgage have their premiums reduced?

Well, since the house is 100 percent yours, the insurance agency will figure that you will take better care of it.

5. Plan for future renovation

When planning to renovate your house, do not neglect to take time to make favorable decisions regarding the materials you use, especially for structures adjacent to your home, such as tool sheds or poultry farms.

If you want to renovate or make additions to your home, you need to consider the materials you will need. Because wood-framed structures are highly flammable, insuring them will be more expensive than using steel-framed or cement structures.

Most homeowners are not even aware that building a swimming pool will increase insurance costs. This is because pools and trampolines or some other potentially dangerous installations can increase your annual insurance cost with up to 10% or more.

6. Regularly conduct policy reviews and comparisons

Regardless of the initial price provided by an insurance agency in their quote, make sure to do some comparison shopping. Check the different group coverage options using credit or trade unions, association memberships, or employers.

You should also learn to compare other insurance policy costs to yours yearly, at least, even after you might have purchased a policy.

Additionally, if you already have an insurance policy, review it from time to time and take note of any changes in the policy that could help lower your premiums.

Also, keep an eye out for changes in your neighborhood that could help lower rates. For instance, if a fire substation or fire hydrant is installed within 100 feet of your home, you could take advantage of this to reduce your premiums.

Periodically assess your most valuable items by doing a home inventory and comparing the total value with what your policy is covering, to avoid being under-insured.

7. Mention that you’re a non-smoker

Smoking is a serious risk factor as it increases the risk of having a house fire. So, if your insurers know that the residents in your home are not smokers, they are more likely to give you discounts.

How Can You Tap Into the Benefits of Homeowners Insurance?

Homeowners insurance is totally worth it if you want to protect yourself, your home, your personal belongings, and your liabilities. Although it will require monthly payments, it will be worth it in the long run.

In addition to providing much-needed protection, it will give you peace of mind, preserve your future, and help to pay for temporary housing if your house becomes inhabitable.

Are you a new homeowner in the Southern California, Treasure Valley (Idaho), and Dallas-Fort Worth area?

Give us a call at Old Harbor Insurance Service so we can discuss your homeowners insurance options.